Fundamental Signals

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

Profile - OBIC Co.,Ltd. (4684.T) - Feb 06, 2026

Feb 6, 2026

Investment, Stocks, Views on Stock

Editor’s Notes

Two days ago, in our “SaaSmageddon” sector note, we highlighted the sharp overnight sell-off across global SaaS names and the market’s growing discomfort with crowded positioning and elevated expectations. OBIC’s recent price action fits squarely into that backdrop. Fundamentals remain strong, but the stock has been temporarily pressured by sentiment rather than execution.

We find OBIC particularly compelling as a direct beneficiary of Japan’s long runway for digital transformation. Despite being a developed economy, Japan continues to lag the OECD average in digital competitiveness, especially in business agility and enterprise-level digital adoption. In the IMD World Digital Competitiveness Ranking, Japan typically places in the 20s globally, well behind the U.S. and Nordic countries. That gap points to structural, not cyclical, demand for core enterprise systems.

Against this backdrop, OBIC stands out as a high-quality, locally entrenched ERP provider with deep switching costs, recurring revenues, and exceptional margins. In a market increasingly skeptical of generic SaaS stories, OBIC offers something different. At current levels, OBIC appears less like a momentum software name and more like a high-quality compounder temporarily caught in a broader valuation and narrative reset.

Business Overview: A Different Kind of Software Company

OBIC is not a typical global SaaS platform competing on user growth or pricing tiers. Its core strength lies in proprietary, deeply localized ERP systems (OBIC7 / OBIC8) tailored to Japanese enterprises, particularly mid-to-large corporates with complex operational needs. These systems are tightly integrated into customers’ accounting, HR, manufacturing, and compliance workflows, resulting in very high switching costs and long customer lifecycles.

The company’s operating model reinforces this moat. OBIC develops its software in-house, sells directly to clients, and provides long-term operational support. This eliminates channel leakage, preserves pricing power, and allows tight control over implementation quality. The result is a business that behaves less like a transactional software vendor and more like an embedded infrastructure partner.

Revenue Mix and Structural Growth Drivers

OBIC’s revenue base reflects both stability and embedded growth optionality:

System Support (52.6% of 9M FY202603 sales): This segment includes cloud solutions, system operations, and maintenance services. It is increasingly recurring in nature and grew over 13% year-on-year, with profit growth outpacing revenue. As clients migrate workloads to the cloud, this segment has become the primary driver of earnings visibility.

System Integration (41.2%): Demand for the OBIC7 Series remains robust, particularly among large and mid-sized enterprises undergoing system modernization. While project-based, this segment continues to grow at a healthy double-digit rate, supported by Japan’s ongoing digital transformation (DX) initiatives.

Office Automation (6.2%): While not core to the long-term thesis, this segment provides incremental contribution and customer touchpoints, though it remains more cyclical and hardware-sensitive.

The key takeaway is that OBIC is steadily shifting toward a higher recurring revenue mix, without sacrificing margins or growth in its traditional integration business.

What are OBIC's Strategic Priorities and Key Growth Drivers?

Current Focus: OBIC is focused on sustaining high-value system proposals, driving growth through cloud solution adoption, maintaining high operational efficiency through its in-house development and direct sales model, and continuous strategic investments in cloud infrastructure and security to ensure long-term stability and service enhancement.

Key Driver 1: Robust Demand for OBIC7 Series ERP: Sustained demand for its integrated business software, particularly the "OBIC7 Series", continues to drive revenue and profit growth in the System Integration segment, especially from large and medium-sized enterprises seeking high-value system construction.

Key Driver 2: Cloud Adoption & Recurring Services Growth: Increasing adoption of cloud solutions and operational support services fuels growth in the System Support segment, contributing to recurring revenue streams and enhancing customer stickiness.

Key Driver 3: Japanese Digital Transformation (DX) Initiatives: The ongoing push for digital transformation and system updates across Japanese corporations, driven by the need for operational efficiency and productivity improvements, creates a persistent demand for OBIC's IT services and software solutions.

Key Driver 4: Efficient Management & Direct Sales Model: An integrated in-house development and direct sales model, combined with efficient management practices, contributes to the company's consistently high operating and net profit margins.

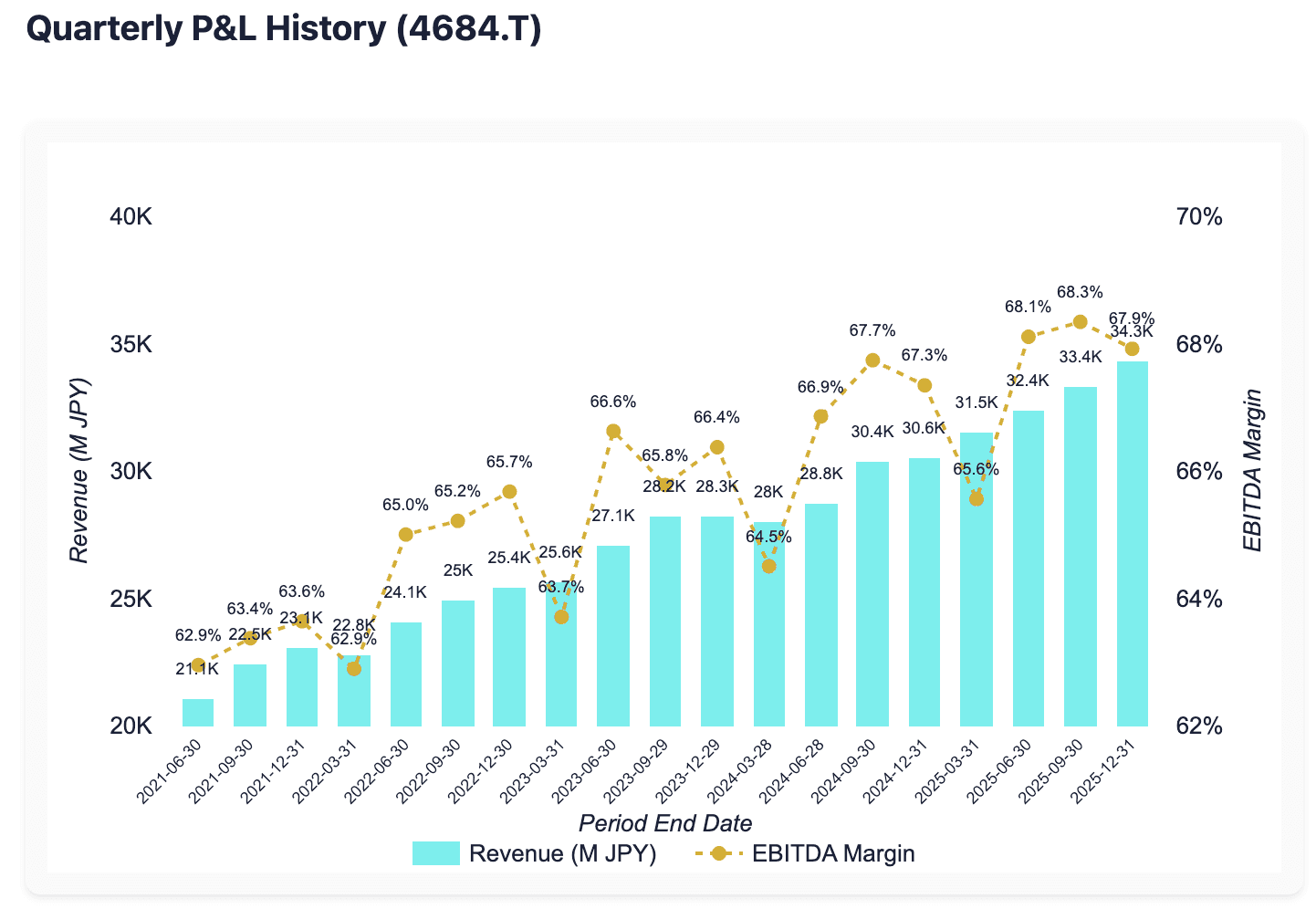

Financial Performance: Consistency at an Elite Level

OBIC’s financial profile remains among the strongest in the Japanese IT services and software universe.

Revenue has grown at a near 10% CAGR over the past two years, while operating margins have expanded from an already elevated base to nearly 65% at the full-year level, and over 66% in the most recent quarter. Gross margins consistently sit near 78%, reflecting both software leverage and disciplined cost control.

Cash generation is equally impressive. Operating cash flow continues to rise, and the balance sheet is exceptionally strong, with nearly JPY 200bn in cash and short-term investments, and no meaningful leverage. This gives OBIC flexibility to invest, return capital, or weather cyclical slowdowns without compromising strategy.

Recent Earnings and Market Reaction

The Q3 FY2026 earnings release was, by most objective measures, strong. OBIC delivered revenue and EPS beats, expanded margins further, and raised its year-end dividend forecast significantly. These results reinforced the narrative of operational discipline and shareholder alignment.

However, the market response was initially negative. The stock sold off sharply following the release, only to rebound the next day. The source of the volatility was not the quarter itself, but management’s decision to maintain full-year guidance.

In a market conditioned to expect upside revisions from high-quality software names, unchanged guidance was interpreted as signaling a softer Q4. This disappointment was amplified by broader negative sentiment toward software stocks, particularly those perceived as exposed to AI-driven disruption or valuation compression.

The subsequent rebound suggests that the initial sell-off was more about expectation management and positioning, rather than a reassessment of OBIC’s underlying business health.

The Core Debate: Execution vs. Expectations

The bull case is straightforward. OBIC continues to grow double digits, expand margins, generate cash, and return capital. Its competitive advantages—local expertise, high switching costs, and integrated delivery—remain intact. From this perspective, recent price weakness looks like an opportunity created by macro and sector noise.

The bear case centers on two concerns. First, whether unchanged guidance implies a genuine slowdown in Q4, particularly in System Integration. Second, whether generative AI and automated migration tools could eventually erode ERP moats by lowering switching costs.

On the latter, skepticism is warranted. OBIC’s systems are not plug-and-play software layers; they are deeply embedded, customized enterprise platforms shaped by local regulation, business practices, and long-term client relationships. AI may enhance productivity, but it is unlikely to materially shorten migration cycles in complex Japanese enterprise environments in the near to medium term.

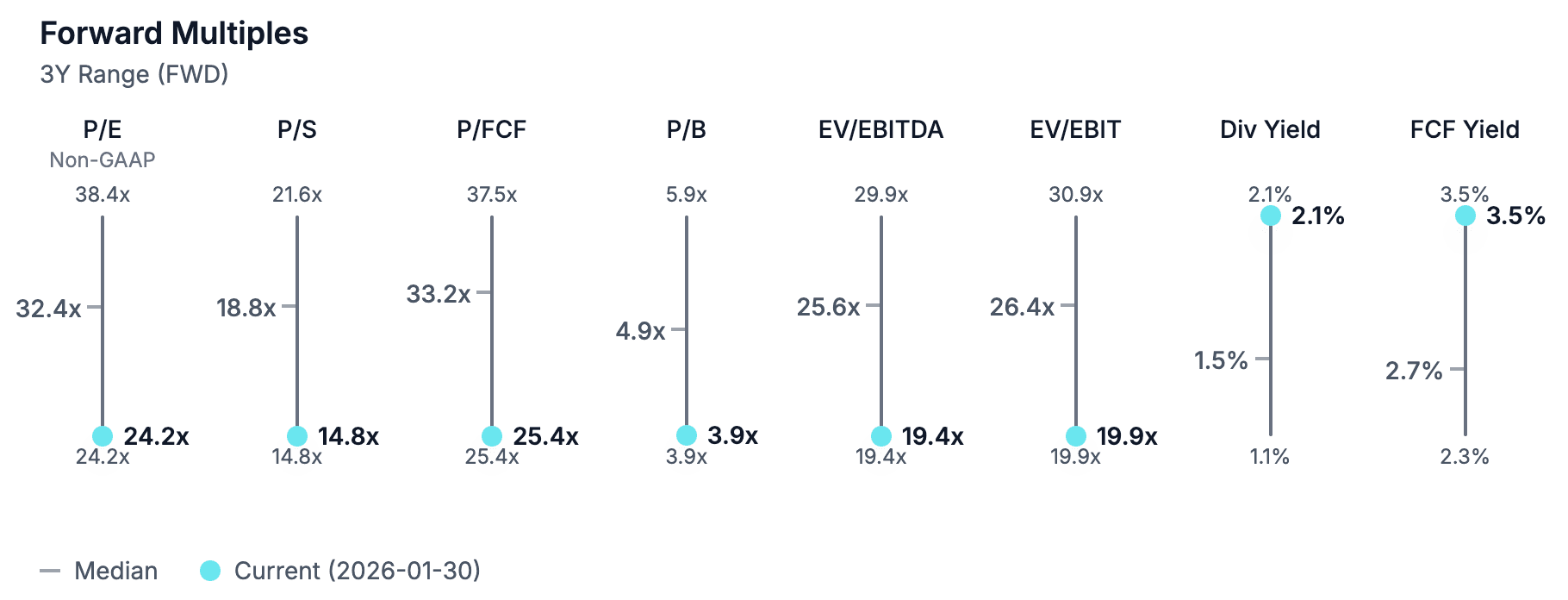

Valuation: A Rare Compression for a Premium Franchise

Following the recent pullback, OBIC now trades at approximately 24x NTM earnings, the very bottom of its three-year valuation range and well below its historical average closer to the low 30s. EV/EBIT and P/B multiples show a similar pattern, while free cash flow yield is now meaningfully above its own historical norms.

This valuation compression is notable given that margins, cash generation, and capital returns are all stronger today than they were during prior periods when the stock commanded higher multiples. From a cycle perspective, OBIC appears to be operating in an early expansion phase, where earnings momentum typically outpaces consensus expectations.

A return to historical valuation levels does not require heroic assumptions. Continued execution, stable demand, and modest improvement in sentiment toward Japanese software would be sufficient to justify re-rating.

What to Watch (Thesis Trackers & Catalysts)

Thesis Trackers:

OBIC7 & Cloud Services Adoption: Monitor growth rates and market penetration for the "OBIC7 Series" and cloud-based offerings within the System Integration and System Support segments.

Operating Margin Trends: Track quarter-over-quarter and year-over-year changes in operating margin to confirm sustained efficiency and profitability.

Shareholder Return Initiatives: Monitor the progress of ongoing share buyback programs and future dividend announcements for management's commitment to capital allocation.

Potential Catalysts:

Further Upward Revision of Guidance: Should current strong trends continue, management may raise full-year FY2026 guidance beyond the already increased dividend forecast, signaling even stronger conviction.

Shift in Analyst Sentiment: A re-evaluation by more "Hold"-rated analysts to "Buy" following sustained strong performance and resolution of AI concerns could trigger a significant re-rating.

Broader Market Rebound in Japanese IT/SaaS: As AI fears normalize or the market differentiates between niche ERP players and broader SaaS, OBIC could benefit from a sector-wide re-rating.

Bottom Line

OBIC represents a familiar but compelling setup: a high-quality compounder temporarily mispriced due to narrative fatigue and elevated expectations. While not immune to macro or sector sentiment, the company’s execution, balance sheet strength, and entrenched competitive position remain difficult to challenge.

For long-term, fundamentally oriented investors, periods like this—when valuation resets while business momentum continues—have historically been the most attractive entry points.

Disclaimer: This content is generated using AI, synthesizing public data (filings, reports, news) and social media (Reddit, X). It may contain errors, inaccuracies, or hallucinations. Nothing herein constitutes financial advice. This newsletter is for informational purposes only; please consult a qualified professional and conduct your own due diligence before making any investment decisions.

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

440 N Wolfe Rd, Sunnyvale, CA 94085, United States

Copyright ©2025 Distilla, Inc. All rights reserved.