Fundamental Signals

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

Pre-Earnings Brief - Netflix (NFLX) - Jul 15, 2026

Jul 15, 2026

Investment, Stocks, Pre-Earnings Brief

Editor's Notes:

As Netflix prepares to report its Q2 2026 earnings tomorrow (July 16, 2026), the dominant narrative surrounding the streaming giant has fundamentally shifted. We are no longer watching a high-stakes, high-growth subscriber land grab. Instead, we are witnessing a crucial strategic pivot: Netflix is evolving into a disciplined, organic compounder.

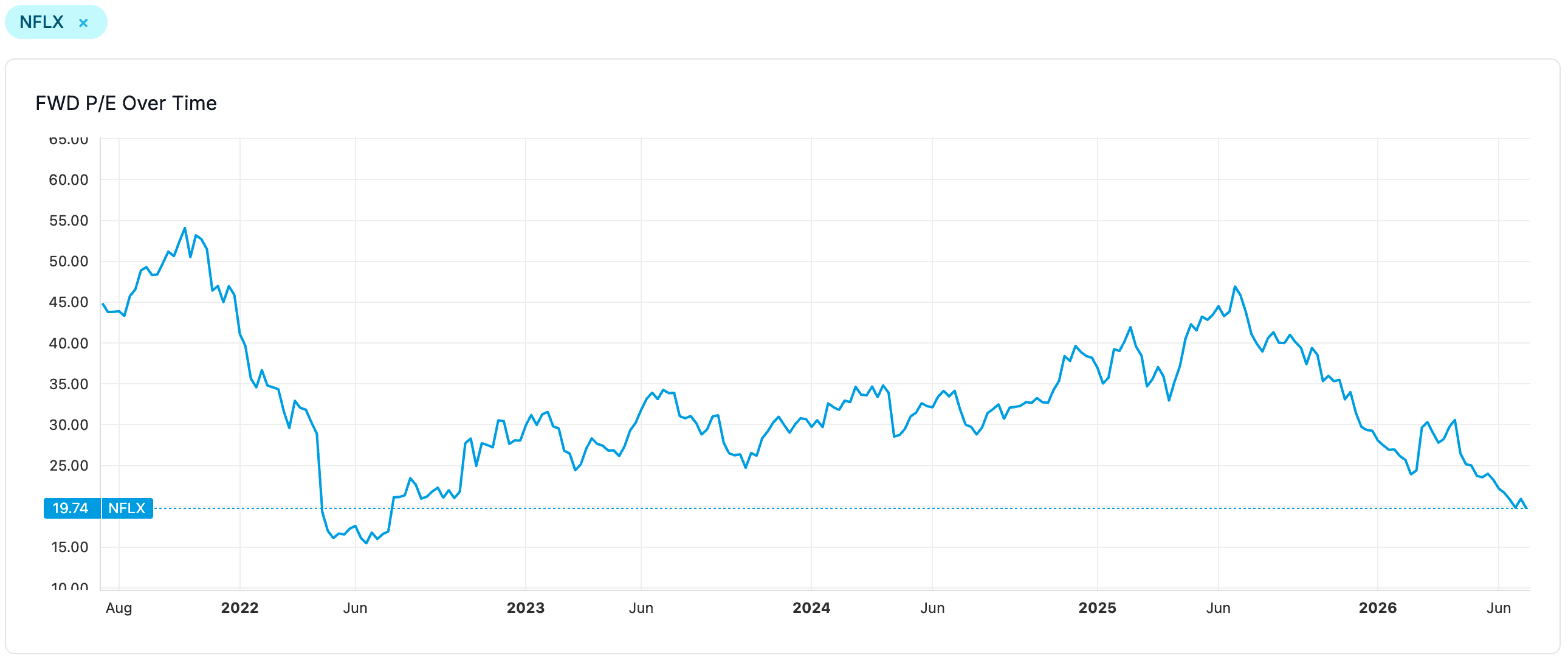

By prioritizing diversified revenue streams—advertising, gaming, live events, and strategic partnerships—and exercising strict capital discipline, management is actively defending its valuation. However, with the stock trading near 52-week lows after a significant 40%+ sell-off over the past year, the market is highly sensitive. Tomorrow’s report will be a critical test of whether this transition can succeed in the face of slowing subscriber growth and intensifying competition.

The Consensus Setup: Numbers to Watch

Wall Street is anticipating an "in-line" quarter, matching management's historically conservative guidance. Here is what the Street expects versus what management has signaled, alongside performance thresholds that will trigger stock volatility:

Metric | Wall Street Consensus | Management Guidance | Beat Threshold | Miss Threshold |

Revenue | $12.58 billion | $12.57 billion | > $12.82B (Guide + 2%) | < $12.31B (Guide - 2%) |

Diluted EPS | $0.79 | $0.78 | > $0.80 | < $0.76 |

Operating Margin | 32.6% | 32.6% | > 32.6% | < 32.6% |

Full-Year 2026 Outlook

Revenue Guidance: $50.7B to $51.7B (representing 12% to 14% growth; 11% to 13% F/X neutral).

Operating Margin Target: 31.5% for the full year.

Free Cash Flow (FCF) Guidance: Recently raised to approximately $12.5B.

Key Performance Drivers & Analytical Context

1. Revenue & Guidance Credibility

Revenue remains the primary indicator of top-line health, especially under the scrutiny of F/X headwinds and pricing actions. Historically, Netflix delivers revenue within 2% of its own guidance. Since management's Q2 guidance ($12.57B) is aligned with the consensus ($12.58B), any significant deviation from this tight range will heavily move the stock. However, a strengthening USD is expected to act as a ~1% headwind this quarter.

2. Profitability & Margins

Netflix typically beats on both EPS and operating income. The notable historical exception was the Q3 2025 EPS miss due to a Brazilian tax dispute, but core operations remain highly efficient. The Q2 operating margin is guided at 32.6%—expected to be the year's highest content amortization quarter—but historical over-delivery suggests room for a positive surprise.

3. Ad-Supported Tier Performance

The ad-tier has emerged as Netflix's primary new growth vehicle, capturing over 60% of Q1 sign-ups in ad-enabled countries and expanding its Total Addressable Market (TAM).

The Target: Management has a target of $3 billion in ad revenue for 2026, aiming to scale to $9 billion by 2030.

The Setup: The ad-supported tier surpassed 250 million monthly active users (MAUs) by Q2 2026. Given consistent outperformance, management's positioning here borders on "sandbagging," leaving room for an upside surprise.

4. Engagement & Churn (The Core Vulnerability)

While Netflix's primary internal quality engagement metric hit record highs in Q1, year-over-year viewing hours growth has decelerated to low-single digits. Following recent price increases, third-party credit card data suggests a larger-than-usual spike in US subscriber churn. Management has historically downplayed total viewing hours in favor of "quality engagement," but internal anxieties regarding tepid engagement have begun leaking to the press.

The Ultimate Debate: Bulls vs. Bears

Bulls Say:

Netflix is seen as an attractive, high-quality compounder, potentially undervalued after a significant selloff (40-44% over the past year), suggesting an oversold setup with reversal potential.

Underlying fundamentals remain strong, indicated by 18% YoY EBIT growth, revenue per member outpacing content spend, and low churn.

New growth vectors are emerging from an aggressive AI strategy, rapid expansion of the ad-supported tier (projected towards $3B by 2026), and diversification into gaming, podcasts, and live events, supported by improving internal engagement metrics and successful initial events.

Management's fiscal discipline, especially in avoiding costly acquisitions, signals a commitment to shareholder value.

Bears Say:

Netflix's core subscriber growth is maturing, increasing reliance on price hikes and unproven new revenue streams.

Competition is intensifying from established players and new entrants (e.g., Meta's Instagram on Samsung TVs, Paramount/Skydance merger).

Recent positive earnings figures (Q1 2026) may have been inflated by one-time payments (e.g., $2.8B WBD termination fee), potentially obscuring underlying cash flow performance and raising questions about earnings quality and sustainability.

Strategic shifts, including past acquisition attempts and increased content spending ($20B in 2026), have led to investor confusion and concerns about strategic direction.

Near-term options market analysis suggests a "slightly bearish" setup with fragility and high volatility expected around the upcoming Q2 earnings.

Key Battleground: The primary battleground will be the Q2 2026 earnings report, specifically the actual operating margin performance against the 32.6% guidance, the growth trajectory of ad-supported tier revenue and subscriber net-adds, and the clarity on free cash flow generation without one-time boosts.

Sentiment Disconnect (Alpha Opportunity)

A Bullish Disconnect is emerging between management's long-term strategic confidence and current short-term market sentiment, particularly among retail investors. While the stock is acknowledged to be near 52-week lows after a significant sell-off, creating an "oversold setup," there remains considerable near-term caution and skepticism, including options analysis indicating a "slightly bearish" setup with "fragility below." Management, conversely, consistently highlights improving internal engagement quality metrics (record high in Q1), strong advertising business growth projections ($3B by 2026), successful live event strategies, and positive gaming impacts, alongside emphasizing fiscal discipline in M&A. This suggests the current market price and bearish sentiment might be underestimating the underlying strategic execution and future growth potential from diversified initiatives.

Surprise Scenarios to Watch

The Genuine Positive Surprise

Ad and Tier Catalysts: Ad revenues pacing well ahead of the $3B 2026 run rate, alongside positive commentary on a rollout of new subscription tiers (e.g., a low-cost, limited-hours tier or high-end binge tier).

Engagement Stability: Lower-than-feared churn rates following the recent price hikes, bolstered by successful live events like the MLB Home Run Derby.

Capital Returns: An increase in share repurchases beyond the current ~$2B per quarter pace.

The Genuine Negative Surprise

Weak Q3 Guidance: Soft forward revenue guidance dragged down by foreign exchange headwinds or post-price hike subscriber loss in 2H26.

Ad Disappointment: Decelerating ad-tier sign-ups or slow ad-revenue monetization against the $3B target.

Strategic Confusion: A pivot back to expensive, debt-laden acquisitions or linear asset buying, coupled with margin compression due to elevated content amortization.

Recent Catalysts (Last 14 Days)

July 14, 2026 | Live Sports Push: Netflix secured global streaming rights for the MLB Home Run Derby, signaling an aggressive expansion into live sports to address engagement deceleration.

July 13, 2026 | Sell-Side Caution: Analysts at Bernstein, Citi, KeyBanc, and Oppenheimer lowered price targets to the $90-$100 range, citing near-term subscriber pressure from the FIFA World Cup 2026, despite maintaining long-term Buy ratings.

July 13, 2026 | Strategic Pivot to Aggregating: Netflix is positioning itself as a content aggregator, partnering with broadcasters like France’s TF1 and exploring live TV integrations.

July 12, 2026 | Targeted M&A: After walking away from WBD assets, Netflix is reportedly in talks to acquire film social platform Letterboxd for ~$250M, favoring low-cost, community-driven engagement over mega-mergers.

July 09, 2026 | Product & Content Launches: Launched the "Netflix Playground" kids app, interactive games ("Unhinged"), and lifestyle video content partnerships (Condé Nast, Hearst) to battle short-form competition from YouTube and TikTok.

Key Questions for Tomorrow's Call

On Engagement Transparency: Given slowing viewing hours, what specific operational metrics is management tracking to measure long-term pricing power and retention?

On New Content Models: How will live TV channels, bundling efforts, and short-form publisher content affect long-term programming costs and operating margin targets?

On Growth Longevity: With analysts lowering price targets on mature-market concerns, what is the clear runway for double-digit revenue growth past 2026?

On Ad-Tier Roadmap: Beyond the $3B target in 2026, what operational milestones (e.g., CPM trends, fill rates) show that Netflix can reach $9B in ad revenue by 2030?

On Capital Allocation: What is the philosophy on M&A post-WBD? Will Netflix continue prioritizing share buybacks over large-scale IP/distribution acquisitions?

Disclaimer: This content is generated using AI, synthesizing public data (filings, reports, news) and social media (Reddit, X). It may contain errors, inaccuracies, or hallucinations. Nothing herein constitutes financial advice. This newsletter is for informational purposes only; please consult a qualified professional and conduct your own due diligence before making any investment decisions.

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

440 N Wolfe Rd, Sunnyvale, CA 94085, United States

Copyright ©2025 Distilla, Inc. All rights reserved.