Fundamental Signals

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

Company Profile - S&P Global (SPGI) - June 05, 2026

Jun 5, 2026

#allen, #distilla

Editor's Notes

When a top investor builds a position during a market pullback, it pays to pay attention. Chris Hohn’s TCI Fund Management recently added to S&P Global, a business showing strong pricing power against tech disruption. While the market feared AI would replace legacy financial data providers, the company is actually securing 35 to 45 percent premiums on its AI-integrated renewals. Because AI models cannot hallucinate legally binding credit metrics or benchmarks, developers are forced to pay for verified data, turning a tech risk into a direct margin driver. For those looking for quality growth at a discount, this setup deserves a closer look.

1. Executive Summary: The Ultimate Valuation-to-Fundamentals Disconnect

In the world of quality-growth investing, finding a wide-moat, high-margin compounder trading at trough valuations while its underlying operational metrics are accelerating is the holy grail. Today, S&P Global Inc. (NYSE: SPGI) presents exactly this rare, highly asymmetric setup.

Over the trailing one-year lookback window (June 5, 2025, to June 5, 2026), SPGI has undergone a significant valuation derating. Its Next Twelve Months Price-to-Earnings (NTM P/E) multiple compressed by approximately 30%, falling from 29.2x to 20.5x. Crucially, this multiple compression did not occur due to fundamental decay; rather, it transpired during a period of robust, double-digit earnings growth. While NTM EPS estimates rose steadily, the stock price declined by -18.54%, opening up an exceptionally wide gap between market pricing and economic reality.

This derating has been driven primarily by exogenous macro headwinds—specifically, higher-for-longer interest rates prompting a massive sector rotation out of financial services and into defensive equities. Sector-wide regulatory anxieties (such as the March 2026 Homebuyers Privacy Protection Act) further dampened sentiment.

However, beneath the macro noise, SPGI’s business engine is humming. Global billed issuance volumes surged +14% year-over-year in Q1 2026 to $1.23 Trillion, propelled by an inevitable, structural $5 Trillion+ refinancing wall that runs through 2029. Simultaneously, SPGI is asserting its immense pricing power, securing 35-45% premiums on its generative AI-integrated data renewals.

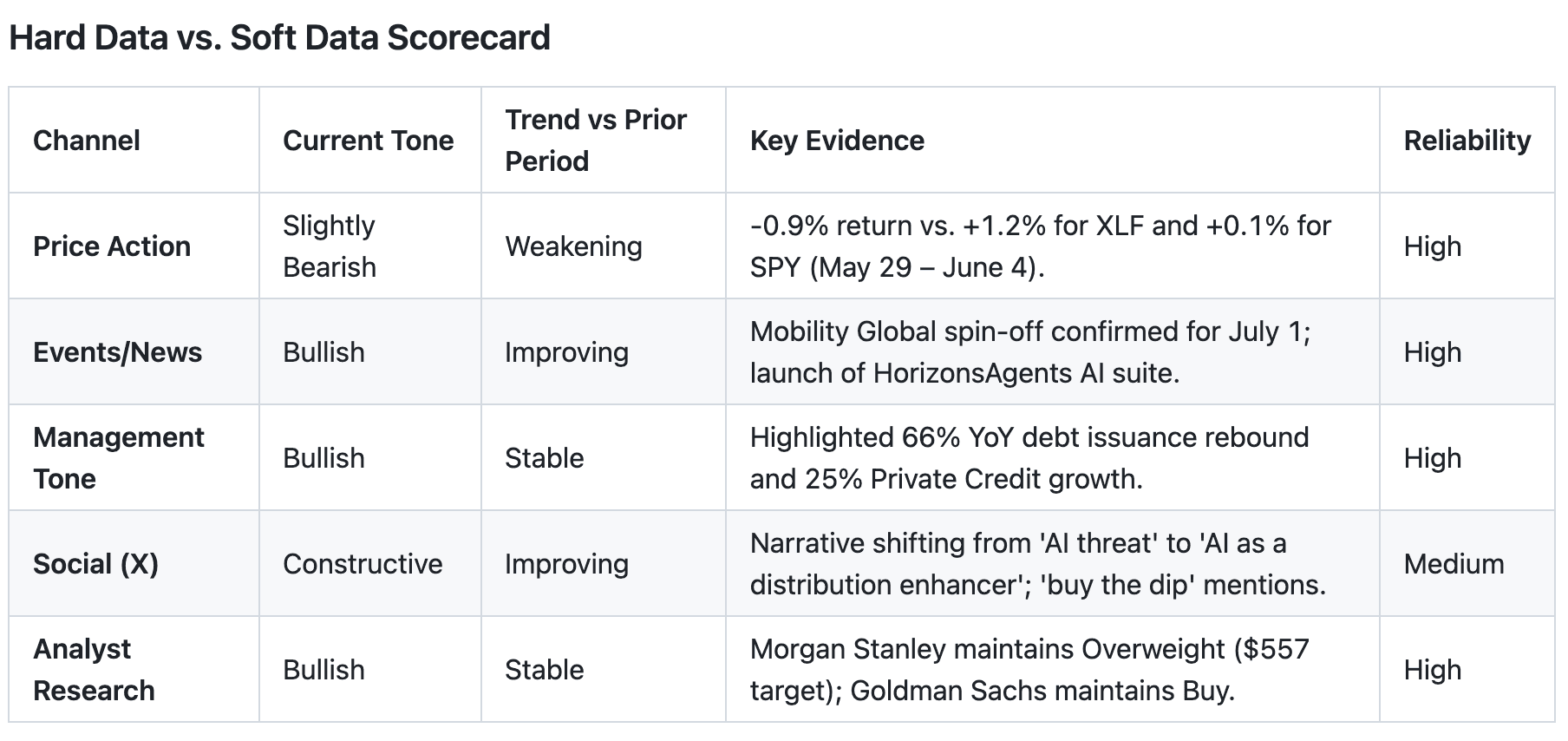

There is a Moderate disconnect between the Bearish Price Action (underperforming the sector by >2%) and the Bullish Narrative (strong earnings, AI product success, and issuance recovery). This suggests the market is still digesting the 'AI threat' narrative while ignoring the fundamental recovery in the Ratings business.

With the stock currently trading in the 12th percentile of its historical one-year range and the 5th percentile of its three-year range (20.5x NTM P/E), the market is pricing in a structural impairment or a sharp cyclical decline. Instead, the leading indicators point to a powerful mid-cycle recovery. We believe this represents a high-conviction "buy the dip" opportunity for medium-term allocators before the imminent spin-off of its Mobility segment on July 1, 2026, acts as a primary catalyst to unlock latent equity value.

2. Multiple Compression Attribution Analysis

This de-rating is not idiosyncratic to S&P Global. It reflects a broader macro-driven multiple regime compression that has plagued the Financial Data and Stock Exchanges sub-sector.

The Drivers of Sentiment Compression

Yield Curve Pressures: The 10-Year Treasury yield remained stubbornly elevated at 4.5% as of early June 2026. Because SPGI is historically viewed as a long-duration growth stock due to its steady compounder status, its multiple is highly sensitive to the discount rate. Additionally, elevated rates initially raised fears of a multi-year freeze in high-yield and corporate debt issuance.

Sector Rotation: The broader Financials sector (XLF) significantly underperformed the S&P 500, posting a modest +5.5% return over the lookback period compared to the broader index's stellar +30.4%. Capital fled financial services in favor of secular AI technology and defensive sectors.

Regulatory Anxiety: The introduction of the Homebuyers Privacy Protection Act in March 2026, alongside heightened global regulatory scrutiny on the "issuer-pays" credit rating model and AI data governance, created a "headline risk" discount.

We rank SPGI's key sensitivities in order of market impact: (1) Interest rates (10Y yield), (2) Debt issuance volumes, and (3) Mobility spin-off execution. While interest rates remain the primary psychological driver of the sector's multiple compression, the secondary driver—debt issuance—has already decoupling positively, leaving the stock fundamentally mispriced.

3. The Structural Moat: A Buffett-Style Business Assessment

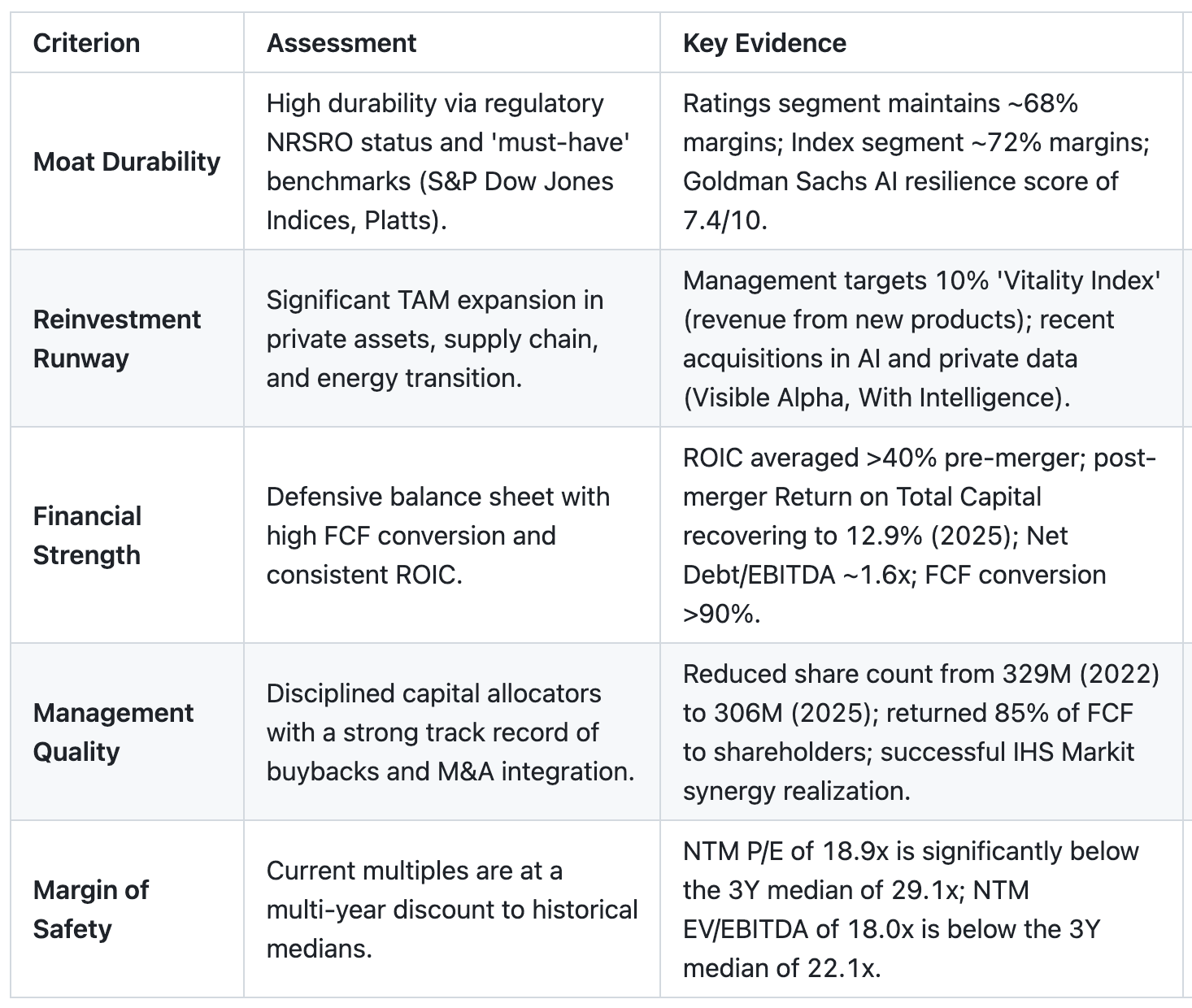

S&P Global operates what Warren Buffett would call a classic "toll-booth" business. To evaluate the durability of this franchise, we rate the company against five core criteria of long-term compounders:

Buffett Criteria Scorecard

Analyzing the Competitive Advantage & AI Resiliency

SPGI's economic moat is primarily defended by high switching costs and intangible regulatory assets. The Ratings segment benefits from institutional mandates; many pension funds and sovereign wealth funds are legally restricted from buying debt that is not rated by an approved NRSRO (S&P, Moody's, or Fitch). In the Indices segment, the S&P 500 is the undisputed backbone of passive investing globally, driving massive network effects.

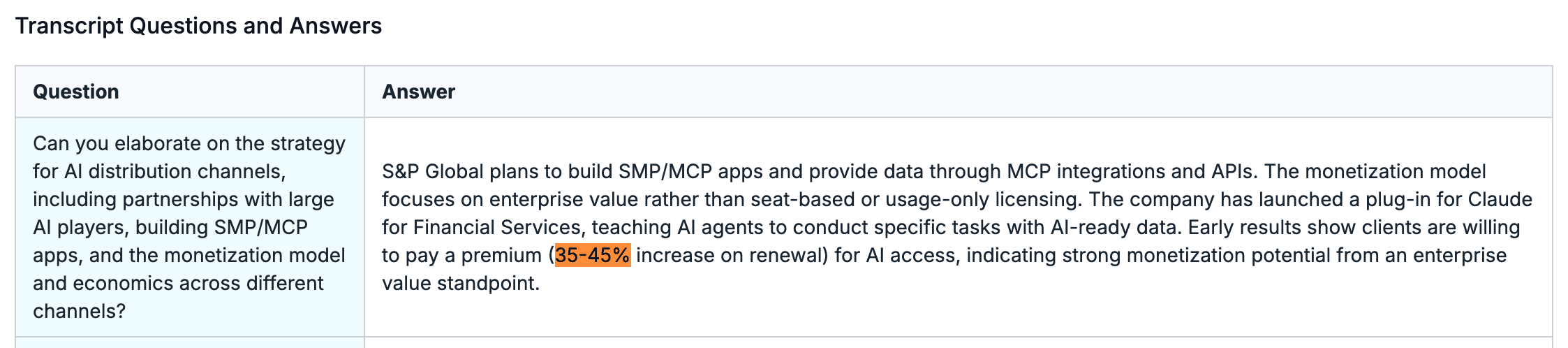

The primary bear argument over the last year has been the threat of Generative AI disintermediating traditional financial data providers. However, this narrative overlooks the value of proprietary data origination. Generative models cannot hallucinate legally binding credit ratings or trade-ready pricing benchmarks.

Goldman Sachs' proprietary AI resilience index scores SPGI an elite 7.4/10, highlighting that AI acts as an efficiency and distribution layer rather than a disruptor. SPGI’s recent launch of the HorizonsAgents AI suite and the Credit Memo Builder inside the Capital IQ Pro platform has proven this. Instead of being disintermediated, SPGI is capturing 35-45% pricing premiums on AI-ready renewals, effectively leveraging its proprietary datasets to drive substantial operating margin expansion.

4. The Micro-to-Macro Cyclical Inflection

While the market continues to price SPGI as if it is in a late-stage cyclical decline, leading operational indicators confirm that the business has entered a 2H-recovery phase.

Company Cycle Position

Phase: 2H-recovery — Aligned with the sector but leading on pricing power. SPGI's Q1 2026 billed issuance (+14%) and Market Intelligence ACV growth (6.5–7.0%) confirm robust demand.

Asymmetry: SPGI is one phase ahead of the market's valuation cycle; while fundamentals signal 2H-recovery, the stock's multiple (20.5x) reflects a 2H-decline scenario.

Margin Cycle: Operating margins are leading the revenue inflection. Q1 2026 adjusted operating income grew to $1.9B, with management targeting >20% run-rate expense reductions in the Enterprise Data Office by 2027.

Current Margins: Operating margin ~45.8% (Q1 2026).

Differentiation: SPGI leads peers due to its 45% global market share in ratings and superior pricing power in AI-integrated workflows (35–45% renewal premiums).

Leading Indicator: Global Billed Issuance Volumes

Credit ratings are highly transaction-dependent, making global billed issuance volumes the single most important leading indicator for SPGI's revenue. In Q1 2026, global billed issuance reached $1.23 Trillion, marking a robust +14% year-over-year increase.

This acceleration is supported by a structural reality: a massive $5 Trillion+ refinancing wall that corporate issuers must address through 2029. High-yield and investment-grade corporate issuers cannot wait indefinitely for interest rates to return to zero; they are beginning to lock in rates, catalyzing a powerful "releveraging impulse" across global capital markets.

In a comparable historical cycle (the 2015–2016 debt issuance recovery), SPGI's stock bottomed exactly one quarter before the leading issuance indicator turned positive. In today's cycle, the stock remains pinned near three-year valuation lows despite the leading indicator having inflected upward four quarters ago. This lag represents a significant market pricing inefficiency.

5. Near-Term Catalysts & The Forward Setup

The asymmetric opportunity in SPGI is supported by several highly visible, near-term events over the next two quarters:

The July 1, 2026, Mobility Spin-Off: SPGI is set to spin off its lower-margin, capital-intensive Mobility segment ("Mobility Global Inc."). This divestiture, following the January 2026 sales of EDM and thinkFolio, completes a multi-year portfolio optimization. Post-spin, SPGI will emerge as a pure-play, high-margin subscription, ratings, and indexing powerhouse. This will likely trigger an immediate sum-of-the-parts re-rating.

The Revaluation Gap vs. Peers: SPGI currently trades at a massive 7-turn discount to Moody's (MCO) on a Price-to-Free-Cash-Flow basis. As the market acknowledges that the "AI threat" has successfully been converted into an "AI monetization enhancement" tailwind, this valuation gap should close.

Earnings Revision Cycle Inflection: Management raised FY2026 organic growth guidance to 9-10% in February. Sell-side consensus models, however, are lagging the fundamental recovery in debt issuance.

Risk Factors to Monitor

Prolonged Interest Rate Volatility: If sticky inflation forces the Federal Reserve to hike rates or maintain the 10Y yield well above 4.5%, multiple expansion could be delayed, forcing investors to rely solely on earnings compounding.

Geopolitical Issuance Freeze: A major geopolitical shock that freezes high-yield debt issuance markets for multiple quarters would temporarily disrupt the ratings recovery cycle.

6. Investment Conclusion: A Strong Overweight Signal

S&P Global Inc. represents a premier business franchise trading at a cyclical discount. The core investment thesis is simple: Fundamental operational acceleration has completely decoupled from compressed valuation multiples.

The combination of pricing power (demonstrated by 35-45% premiums on AI workflows), robust macro tailwinds (the $5T refinancing wall), and an impending corporate catalyst (the July 1 Mobility spin-off) provides a highly favorable risk-reward profile. We recommend that investors take a serious look at SPGI at current levels to capture both structural earnings compounding and significant multiple expansion as the market realizes the durability of this financial powerhouse.

Disclaimer: This content is generated using AI, synthesizing public data (filings, reports, news) and social media (Reddit, X). It may contain errors, inaccuracies, or hallucinations. Nothing herein constitutes financial advice. This newsletter is for informational purposes only; please consult a qualified professional and conduct your own due diligence before making any investment decisions.

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

440 N Wolfe Rd, Sunnyvale, CA 94085, United States

Copyright ©2025 Distilla, Inc. All rights reserved.