Fundamental Signals

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

Company Profile - Dai Nippon Printing (7912.T) - Apr 15, 2026

Apr 15, 2026

Investment, #distilla, Stocks, Company Profile

Editor's Notes

We are taking a closer look at Dai Nippon Printing Co., Ltd. (7912.T) after highlighting it as a potential idea in our newsletter today. The core thesis is its strategi pivot from a legacy printing firm into a vital supplier for advanced semiconductor materials and OLED displays. This strategic shift allows the company to capitalize on secular growth in AI, IoT, and electric vehicles while the broader market is still underpricing its early stage earnings recovery.

Beyond the technology pivot, DNP is perfectly positioned to benefit from the structural governance changes sweeping across Japan. As corporate pressure mounts to improve shareholder value and deliver strong capital returns, the company has a clear catalyst for a broader structural revaluation.

Business Snapshot

DNP is a diversified Japanese conglomerate leveraging its high-precision manufacturing expertise from printing to expand into high-tech electronics, packaging, and digital communication services. Its primary moat lies in proprietary patents and deep customer relationships in display/semiconductor components.

Narrative & Market Debate

The dominant market narrative for DNP revolves around its transformative strategic pivot from a traditional printing company to a diversified, high-tech player deeply embedded in the AI and semiconductor supply chain. This shift, highlighted by its "Strategic Shift to Diversified Technology and Sustainable Solutions" (March 27, 2026) and "New Mid-Term Management Plan" (March 17, 2026), aims to capitalize on megatrends like digitalization and sustainability. Institutional actions, such as BlackRock Japan increasing its stake to 7.62% and Nomura/Mizuho reporting major stakes as of March 31, 2026, signal growing confidence in this new direction, leading to a +4.28% price rise on April 8, 2026.

The key debate centers on whether DNP is a significantly undervalued "hidden gem" or if it remains burdened by its legacy. Bulls argue DNP is a crucial high-tech player in AI/semiconductor (e.g., photomasks, NIL templates for 1.4nm, OLED FMM) with robust fundamentals, strong shareholder returns, and partnerships with industry giants (TSMC, Intel, Samsung), poised for substantial growth from its electronics segment. Bears, while acknowledging the pivot, remain cautious, citing historical reliance on a declining legacy printing business, inherent cyclical risks in semiconductors, and potential execution risks in transitioning to high-tech.

Competitive Position

DNP exhibits strong competitive positioning and appears to be outperforming key domestic rivals while benefiting from industry tailwinds. In packaging, DNP's strategic focus on recyclable/bio-based materials and advanced solutions is validated by competitor Amcor plc's (AMCR) success in sustainable packaging and expansion into high-growth health/nutrition end markets. The robust demand for sustainable packaging, with retortable mono-material pouches growing at a 10% CAGR, confirms DNP's strategic importance in this area.

Crucially, DNP is demonstrating superior operating performance compared to its domestic peer, TOPPAN Holdings Inc. (7911.T). While TOPPAN reported a -15.1% decline in operating profit, DNP achieved a +21.8% YoY operating profit growth in the same period (Q3 FY2026). This suggests DNP benefits from better cost management, product mix, or market positioning, despite both companies projecting similar +4.1% revenue growth for FY2026. Furthermore, strong industry outlooks, such as the 12.4% CAGR for glass interposers (AGC Inc.) and 14.4% CAGR for digital textile printing (Seiko Epson Corporation), validate DNP's strategic expansion into advanced materials and high-value-added technologies.

Value Chain Signals

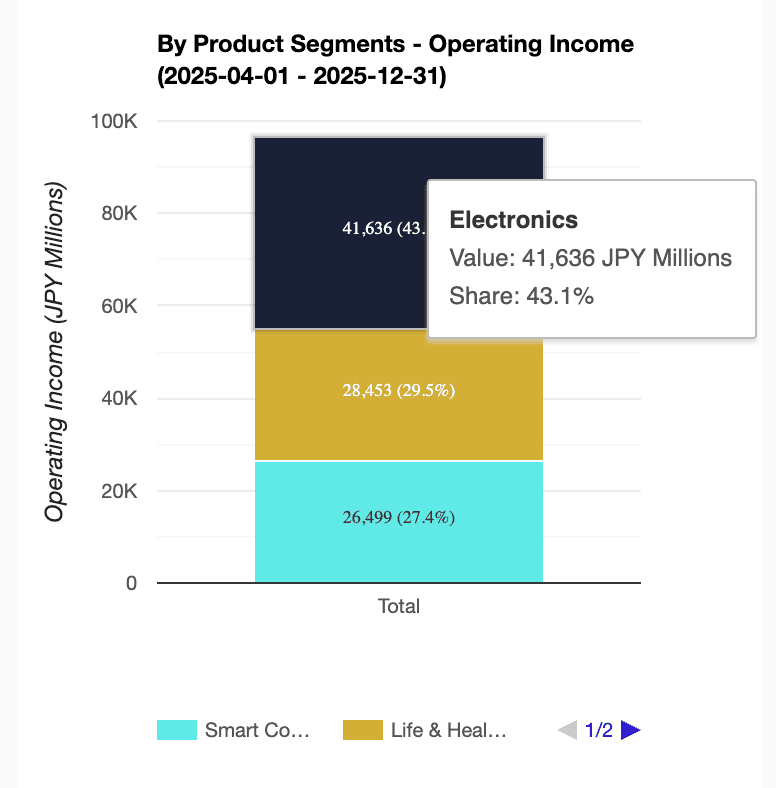

The most material value chain signal is the significant and growing demand for advanced and sustainable packaging solutions. The Japan barrier tube packaging market, where DNP is a key player, is projected to grow from USD 733.3 million in 2025 to USD 1,300.3 million by 2035 at a 5.9% CAGR, driven by pharmaceutical innovation and premium cosmetics. This directly impacts DNP's Life & Healthcare segment (~30% of sales). Furthermore, the industry-wide increase in crude oil and raw material prices, as evidenced by TOPPAN's reduced packaging operating profit forecasts, implies potential margin pressure for DNP's packaging business, necessitating effective cost management or pass-through strategies. Conversely, the robust demand in advanced electronics (AI, foundry-logic, memory, advanced packaging) highlighted by AGC's glass interposer growth provides a strong tailwind for DNP's Electronics segment.

Recent Catalysts

2026-03-17: New Mid-Term Management Plan: DNP announced aggressive financial targets for FY2029 (¥130B operating profit, 9% ROE) and FY2032 (¥150B operating profit, 10% ROE), along with strategic investments in mobility, semiconductors, information security, and photo imaging.

2026-03-26: Strategic Pivot & Product Launch: Introduced new recyclable flexible packaging solutions aligned with circular economy regulations and announced a shift toward a diversified technology provider model, emphasizing Life Sciences and IoT-enabled smart packaging.

2026-03-31: Treasury Stock Cancellation: DNP planned a significant share cancellation of 85 million shares (16.21% of outstanding) for March 2026, enhancing shareholder value and capital efficiency.

Investment Case

Upside

Dominance in High-Growth Tech Niches: Leading positions in photomasks, OLED FMM, nano-imprint lithography templates for 1.4nm logic, and Li-ion battery pouches, all benefiting from AI, IoT, and EV megatrends.

Accelerating Margin Expansion: Gross margins are projected to reach ~24.8% by FY2028 from ~20.4% in FY2023, driving significant operating leverage with 21.8% YoY operating profit growth in FY2026 Q3.

Strategic Shareholder Returns: The cancellation of 16.21% of outstanding shares in March 2026, combined with a strong net cash position, enhances capital efficiency and provides a solid floor for valuation.

Risk

The single biggest risk to the thesis is the inherent cyclicality and potential for slowdowns in the semiconductor and electronics markets, which could materially impact demand for DNP's high-tech components if AI adoption falters or global trade tensions escalate.

Valuation

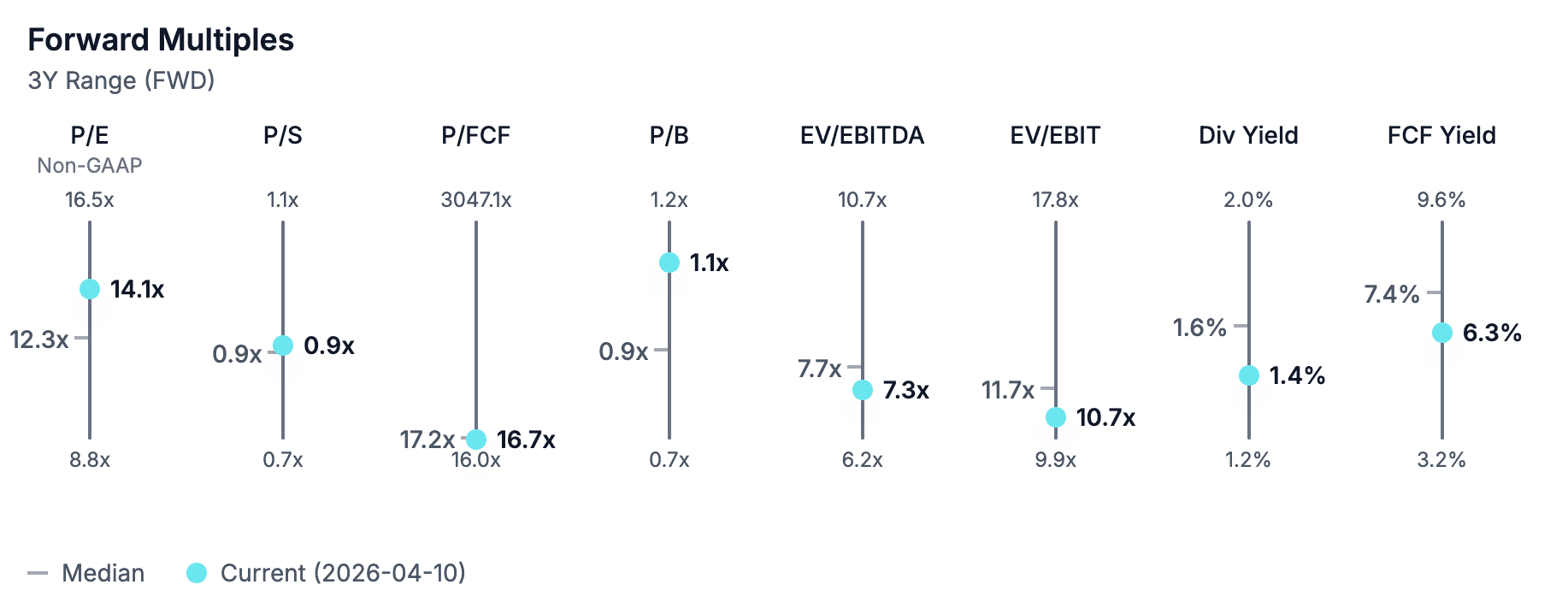

DNP trades at a NTM P/E of 14.1x, NTM P/B of 1.1x. The valuation appears conservative given the accelerating operational performance and dominant positions in high-growth tech segments, suggesting potential for a multiple re-rating as its strategic transformation unfolds.

Disclaimer: This content is generated using AI, synthesizing public data (filings, reports, news) and social media (Reddit, X). It may contain errors, inaccuracies, or hallucinations. Nothing herein constitutes financial advice. This newsletter is for informational purposes only; please consult a qualified professional and conduct your own due diligence before making any investment decisions.

You are in good company - veterans at top funds are reading.

Don't miss a key signal and start reading today!

440 N Wolfe Rd, Sunnyvale, CA 94085, United States

Copyright ©2025 Distilla, Inc. All rights reserved.